DZ BANK Research - Outlook 2024: "Soft landing" in Europe and the USA - but recovery only sluggish / Wages keep inflationary pressure high / Bond yields fall again / DAX reaches 17,500 points

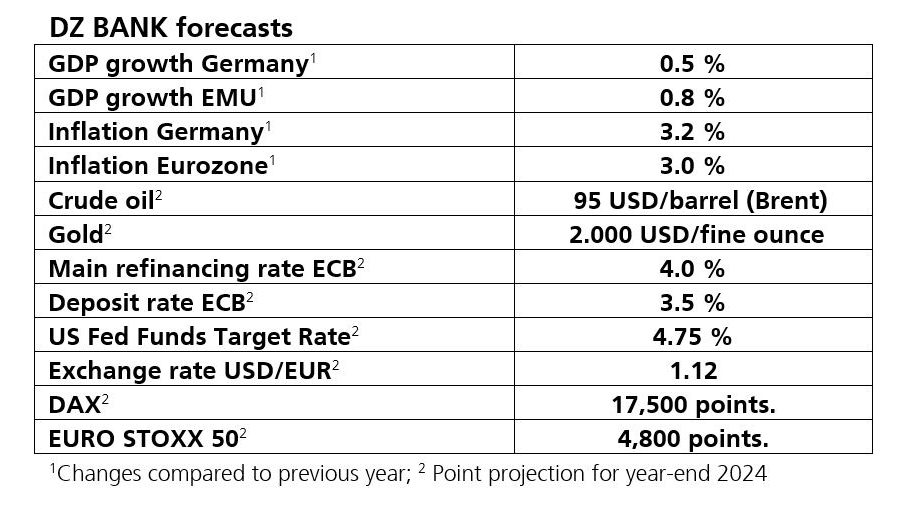

DZ BANK Research has mixed feelings about the coming year. Analysts expect a further decline in inflation in the Eurozone and in Germany. However, the ECB target will once again be clearly missed. The economy also continues to cause concern. In Germany, DZ BANK experts expect GDP growth of 0.5 percent. The US economy grows by 1.5 percent. At least: A "hard landing" will not become a reality. Experts expect interest rates to be cut slightly in the second half of the year, both in Europe and on the other side of the Atlantic. Bond yields should therefore fall. The major share indices will remain unimpressed by the volatile global situation in 2024. Analysts are therefore forecasting new records for the DAX at 17,500 points and the S&P 500 at 4,800 points.

Following the corona virus pandemic and the start of Russia's war of aggression against Ukraine, the end of the year was also characterised by great uncertainty. Numerous central banks combated historically high inflation with an unprecedented turnaround in interest rates. The European Central Bank alone has raised its interest rates ten times in a row since July 2022. In combination with a disappointing economy in China and only slowly falling inflation, the restrictive central bank policy caused an economic belly ache, particularly in Germany. The export-dependent German economy even slipped into recession. Global growth is also expected to be low by historical standards at 2.9%. The war in the Middle East is causing additional uncertainty, particularly with regard to energy prices.

Despite disputes over the US budget, the world's largest economy is coping comparatively well with the multi-crises. Even the strict monetary policy could not prevent construction investment from increasing recently. In addition, brisk consumption is currently ensuring strong growth. In the third quarter, GDP rose by 4.9% compared to the previous quarter. However, this pace is unlikely to be maintained. DZ BANK Research forecasts growth of 1.5 percent for 2024. Analysts see inflation at three percent. The experts believe that the first key interest rate cut is possible from the second quarter - the economists expect a total of three steps of 25 basis points each.

According to DZ BANK Research, the direction in which the US economy develops will also depend on the outcome of next year's presidential election. "US economic policy must find a way out of its very expansionary course, which is associated with unsustainably high deficits in the long term," says chief economist Michael Holstein. At the same time, the presidential election will lead to a phase of uncertainty as to whether the future majority situation will even allow clear priorities to be set. In addition, a new old President Donald Trump could torpedo existing trade agreements.

Falling inflation but weak economic development in the Eurozone

Inflation has also weakened in the Eurozone. In October, it fell below the three percent mark again for the first time. However, the recent downward trend is due to the high energy price levels of the past year. Analysts therefore expect inflation to fall only slowly. In addition, price pressure on services will remain high in 2024 due to wage increases. Experts expect inflation to rise by three percent in the coming year. As food prices are also continuing to rise, a rapid recovery in consumption is not to be expected. There is also a lack of external economic impetus, which is why EMU GDP is only likely to grow by 0.8%.

Germany is barely making any headway: Package for SMEs gets bigger

According to a special DZ BANK survey, almost 50 percent of SMEs see Germany as the "sick man" of Europe. This is mainly due to expensive energy and a overburdening bureaucracy. Added to this are economic concerns. "We only expect an increase of 0.5% for 2024," explains Michael Holstein. He attributes the low growth in particular to the continued tense global economy - strong export business at pre-corona levels is therefore unlikely. There is also a weak propensity to buy among consumers.

ECB: Less restrictive, but vigilant

DZ BANK Research does not expect the European Central Bank to tighten interest rates any further. However, the current restrictive interest rate level is likely to be maintained for a longer period of time. "The ECB is proceeding cautiously with a close eye on inflation. This vigilance is well placed. The monetary policy turnaround will not come until the fourth quarter of 2024," Christoph Kutt says, Head of Fixed Income Research. The expert therefore expects only two cautious interest rate cuts of 25 basis points each, which will be implemented by the central bank between October and December.

Bond markets without a central bank nanny: Reality test for issuers

Fixed income has made a return this year and will be more than a stabiliser in the portfolio in 2024. "The yield on ten-year US bonds broke through the five percent mark in October for the first time since 2007. Corporate bonds with investment grade status also offer similar levels," explains Christoph Kutt. In view of the significant fall in inflation, this is once again a good option for investors. These levels should now be secured, as interest rate cuts from the second half of the year are likely to drive yields down again somewhat in the run-up. The increasing attractiveness for investors - without central banks as major buyers - is also putting issuers under pressure. "The tighter monetary policy is a reality test for the entire market," says Kutt.

High interest rates and little growth: Stock markets nevertheless set new records

In both Germany and the USA, the stock market was not unaffected by the many crises in 2023. A weak economy and competition from bonds will continue to influence share prices in 2024. Chief equity strategist Sven Streibel nevertheless expects new records for the major indices. "Investor sentiment is at its lowest point. If the bad news clears up just a little, there is enormous potential for positive surprises. This speaks in particular for favourable European cyclicals," says Streibel. The expert also believes that the "resilient" major US tech stocks are still a safe bet. "Big tech is a growth centre in a low-growth world," explains the analyst. He forecasts 17,500 points for the DAX and 4,800 points for the S&P 500 by the end of the year.

Despite the positive outlook for equities, Streibel stresses that there is no promise of success across the board: "Targeted regional and sectoral stock selection is becoming a success factor in the investment strategy." At sector level, DZ BANK Research recommends energy stocks and insurers, for example. European car manufacturers should also benefit from an economic recovery.